Did you know that 9.55% of the student loans extended by public sector banks were declared as non-performing assets for the financial year 2021? Source

It is a common telltale in India to hear about deserving students being denied entrance to higher education institutions owing to financial difficulties. Many of these students are already in debt due to expensive tuition fees incurred due to coaching.

Hence, it becomes difficult for them to pay further expenses at the counselling stage or the costs incurred after admissions such as tuition fees and living expenses.

The good news is there is an alternative to all of this- An income share agreement (ISA).

What is an Income Share Agreement

An income share agreement (ISA) is an alternative way to pay for college that provides funding in exchange for a percentage of a student’s post-graduation income for a set period.

An income share agreement (ISA) is a contract in which a student receives upfront funding for higher education in exchange for a specified proportion of their earnings after the course is completed. Repayments do not begin until the borrower earns a minimum threshold amount, and repayments are automatically suspended during periods of unemployment.

Theoretically, the concept of ISA is easy. However, there are complications because different facilitators have varying amounts and conditions. These complications include the percentage of the student’s income that the school takes, the overall cap on the amount that must be paid back, and the period for repayment.

Following are the various terminologies associated with Income Share Agreement at Masai.

Now, the minimum income threshold is the minimum income set by the school below which a student won’t be asked to make “any” payments.

The income share percentage is the fixed percentage of the student’s income that needs to be paid to the school if their income exceeds a specified threshold.

A question may arise here:- “What if other students are making a much higher income than the threshold? Will they be paying too much based on the fixed share?”

To tackle this issue, there is a payment cap which is the maximum amount a student will have to repay under any circumstances. It ensures that students earning different amounts as salaries eventually pay the same amount to the school. Then there is a payment period or payment tenure after which the ISA contract terminates and the student is released from all obligations.

Why is there a need for Income Share Agreement in Higher Education?

The rising expense of higher education has made it extremely difficult for financially disadvantaged families in India to allow their children to study. Pursuing a college degree in general courses costs Rs 5,240 per student in rural areas and Rs 16,308 in urban areas, which is more than three times the rural average.

Engineering normally costs Rs 1.25 lakh per year or Rs 5 lakh for a four-year course. The course fee in premier colleges like IIT or BITS Pilani goes as high as 10 to 15 lakh for the entire duration of 4 years.

While AIIMS might come as a relief for medical students by providing a limited number of seats at very nominal fees, the costs incurred can go as high as 1 crore when students turn to private institutes.

A 2-year residential PGP programme at a prestigious institute in India will cost between Rs 12 and 15 lakhs. B-schools that participate in GMAT often accept more experienced students and charge more fees. Expect to spend an average of Rs 20-25 lakhs in India and around Rs 70 lakhs abroad.

Although many of these institutes provide scholarships, they are few and put in place just for poor families. Many students secure education loans at 7-16 percent interest per year to pay for their education expenses.

This is where Income Share Agreement in India comes into the picture.

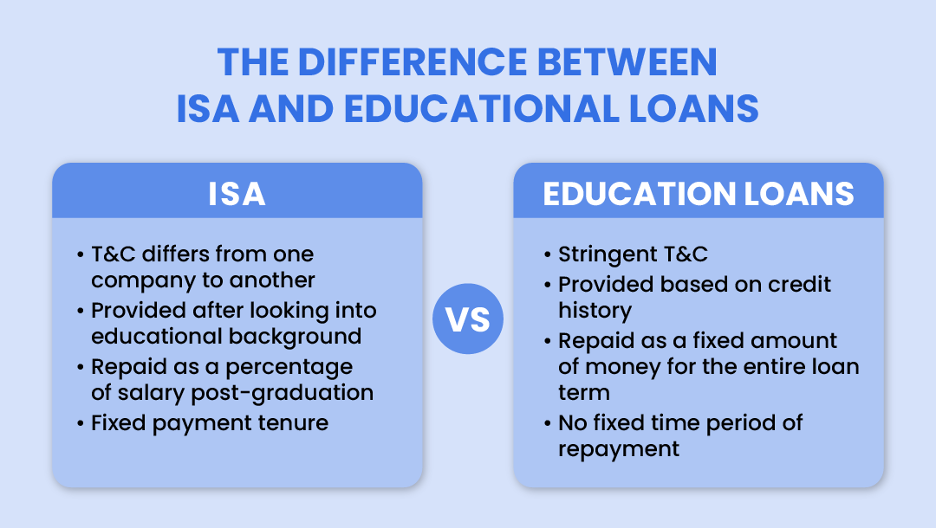

What makes ISA different from student loans?

Education loans and ISAs are both fantastic resources for students in need who want to alter their future. The two systems’ main differences are seen in how they operate.

A student loan is a debt that must always be repaid; in contrast, an ISA is an investment in the student’s future. An investment that is entirely reliant on a student’s achievement and is only repayable if they land the job.

ISAs differ from student loans in the following ways:

Variable terms: Education loans are strictly regulated, and all loans follow the same structure and repayment procedures. However, ISAs function differently. Because they are issued by separate companies, the terms and conditions may differ from one another.

Risk-based classification: While education loans have the same rates and terms for all borrowers, Income Share Agreements determine them based on the borrower’s major, degree track, university, and academic record when determining eligibility and terms.

In terms of education loans, the lending parties take a look at the borrower’s credit history and income to establish eligibility and interest rate.

Repayment structure: Repayments under a shared income agreement are a percentage of a student’s income. As students’ income grows, so will their payments. The payment for student loans on regular repayment plans remains the same for the term of the loan.

Limitations of ISA

Income Share Agreements are not operating at a scale as large as student loans. As a result, they are less prevalent. Currently, ISA is only being offered in a select few institutions and boot camps throughout the world. There aren’t many courses offered under these agreements because of this. ISAs are anticipated to grow quickly and spread widely in the coming year, though, given the student debt issue and the several advantages they have over student loans.

ISAs are not regulated. They lack a centralised set of guidelines for how to conduct themselves. As a result, despite operating under the same general premise, each institute offering ISA has a different programme structure and set of payment terms. Students become confused as a result of that. Before signing the agreement, it should be carefully reviewed.

ISA is not for everyone. People unwilling to work after completing graduation, looking to pursue higher education after the ISA program, and not yet convinced about the industry or field of work they want to choose should not consider opting for ISA as this will only add an extra financial burden on their shoulders.

Final Thoughts

The current state of the educational system has significant deficiencies, and ISA programmes have been quickly arising with a promise to remedy these gaps. And so far, whether it is job placement or overall career progress, they have fulfilled this promise. They frequently have a strong framework for specialised learning in place, which significantly improves the chances of finding employment.

About the Author: This is an invited post from Nitish R Sonu. He is a Content Associate at Masai | Stamurai |. Self-proclaimed storyteller | The one who dilutes complex topics into simple lucid ones